Home » Banking & Finance » SME Chamber of India demands review of issues related to banking towards MSME sector

Hey, like this? Why not share it with a buddy?

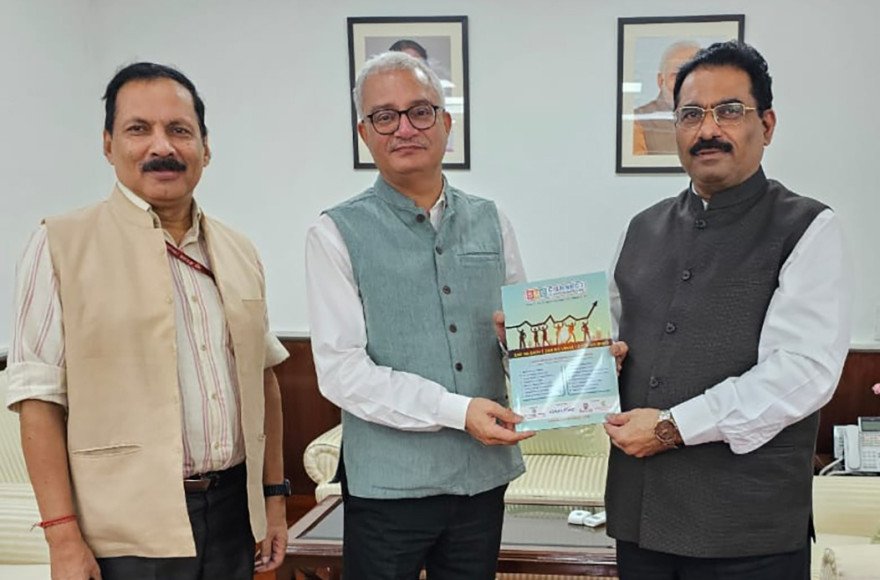

Mr. Chandrakant Salunkhe, Founder & President, SME Chamber of India & Federation of Indian SME Associations had met Dr. Vivek Joshi, Secretary and Dr. Bhushan Kumar Sinha, Joint Secretary of Department of Financial Services, Ministry of Finance, Government of India to present suggestions and Grievances pertaining to SME sector and presented Activity Report of the Chamber on 28th May 2024 at New Delhi

SME Chamber of India has demanded to take the review of financial institutions related to financial support & services, which have not been achieved the targets due to many reasons for the last 2 years and the Chamber has submitted its Memorandum to Dr. Vivek Joshi, Secretary, Department of Financial Services, Ministry of Finance, Govt. of India through Shri Chandrakant Salunkhe, President of Chamber & Federation of Indian SME Associations (FISA) as well as business activist and who has been on the forefront for the last 31 years to provide support and guidance for the business growth and taking up their issues and grievances with the appropriate Government Departments to secure the interest of MSME sector. Mr. Salunkhe has submitted 25 points agenda to review, transform and implement the various facilities towards the credit flow for MSME sector, so that they can put more efforts for marching towards “Viksit Bharat”. SME Chamber of India has been putting efforts for the empowerment of SME sector for the last 31 years to achieve economic & industrial growth of the nation, export promotion, employment generation and interacting with the Government officials and regulatory bodies for policy framework change & its speedy implementation.

India’s 6.33 crores MSMEs have been putting efforts for the growth of Indian economy, contribute for the industrial output, exports and generation of large employment as well as playing vital role for marching towards “Viksit Bharat” but have not been provided timely and affordable financial supports by the financial institutions/banks for business growth, expansion, diversification and working capital requirements. As per RBI data published in their annual report for the financial year 2023-24 on 31st March 2024 shows that 2.61 crores MSMEs are having outstanding amounts of Rs.26 lakh crores till 31st December 2023. This data shows that 60% MSMEs are still struggling to avail financial facilities from the banking sector for many reasons. The increase in credit to micro, small and medium enterprises (MSMEs) was robust at 14.1 per cent, supported by the availability of collateral free loans. On a y-o-y basis, the outstanding credit to the MSMEs by SCBs expanded by 20.9 per cent during 2023-24 (up to end-December 2023).

In order to facilitate formalisation of informal micro enterprises (IMEs) which were not able to register on the Udyam registration portal due to lack of mandatory documents such as permanent account number (PAN) or goods and services tax identification number (GSTIN), the Ministry of Micro, Small and Medium Enterprises (MSMEs), Government of India (GOI) had launched an Udyam assist platform (UAP). Accordingly, a circular was issued stipulating that IMEs with Udyam assist certificate shall be treated as micro enterprises under MSMEs for the purposes of priority sector lending (PSL) classification. Currently, Udyam Registration of MSMEs comprise micros 2.56 crores, small 7.05 lakhs and medium enterprises 67,247 only and providing employments to 17.28 crores. Also, as per the data of Ministry of Company Affairs, total number of registered companies are 26.5 lakhs. In that 10 lakhs are closed, sick or dormant and only 5,600 are foreign entities registered in India. That means more than 6.25 crore enterprises and 4 crores self-employed enterprises which are not registered under any Central Government agencies but some of them have registered as a partnership and proprietorship firms. These enterprises can be approached as a potential customer for the financial institutions for extending their credit facilities to achieve the targeted growth.

In Union Budget 2023-24, the Government announced the revamping of credit guarantee scheme for micro and small enterprises with effect from April 1, 2023, with an infusion of ?9,000 crores to the corpus to enable additional collateral-free guaranteed credit of ?2 lakh crores and the reduction in the cost of the credit by about 1 per cent. Besides, the limit on ceiling for guarantees has been enhanced from ?2 crores to ?5 crores. Small and medium enterprises (SMEs) segment exhibited exuberance with 197 SME IPO/ FPO issues garnering ?6,122 crores in 2023-24, as compared with 125 SME IPO/FPO issues mobilising ?2,333 crores a year ago.

SME Chamber of India has invited the issues & suggestions from Members of SME & manufacturing sectors related to banking sector for financial facilities, improvement of strategies to enhance credit flow and revival of sick units as well some practical approach by the bankers to provide breathing space to the MSME sector. The Chamber has observed that many MSMEs are not in the comfort zone, therefore the micro enterprises are taking 8 to 10 years to become small enterprises & small enterprises having turnover upto Rs.50 crores are struggling for 5 to 6 years to become medium enterprises, to enhance their turnover and medium enterprises are also struggling for many years to become emerging mid-corporates, only because of lack of financial support, high rate of interest, negative & lack of approach and soft corner for the revival of struggling units by the banks & negligence.

Mr. Salunkhe has requested Dr. Joshi to look into the following matters and recommend to the Governor, RBI & Indian Banking Association (IBA) to review the suggestions to give attention on a priority basis to provide timely credit facilities & level playing field to MSME sector to accomplish the dream project of Hon’ble Prime Minister to ‘Make India as a Manufacturing Hub of the World’ and a largest economy.

Recommendations and suggestions:

- To organise joint economic survey of SME sector & do SWOT analysis, evaluate the hurdles for availing credit facilities for their business growth and expansion.

- To enhance credit facilities without collaterals upto Rs.10 crores for small enterprises for buying machines, equipment and also for working capital requirements.

- To set up permanent Standing Committee to review credit flow towards MSME sector under the Chairmanship of Dy. Governor of RBI, banking services, including heads of all banks, office bearers of leading national level organisations, rating agencies and the State Governments representatives to continue the discussions and implement the action plans for the benefit of MSME Sector.

- To advise the MD and ED and CGM or GM handling MSME department to make available to meet the customers, office bearers of the various associations and victims of lack of services of the bank once in a month with appointment on a priority basis to under the major problems and grievances impacting to one and all enterprises.

- To give exemption to submit monthly stock and debtors’ statements from micro & small enterprises, are enjoying facilities upto Rs. 5 crores and consider half yearly.

- To achieve 2 trillion dollars exports, PSBs should focus on providing trade and supply chain finance on a priority basis and at the affordable rate of interest.

- If any enterprise is not happy with the services or cooperation from any financial institutions, they should be allowed to switch on to other institutions to enjoy the similar facility as a mobile number portability system.

- To review before defining any enterprise as a wilful defaulter enjoying facility upto Rs.5 crores and clarification to be invited from the similar enterprises with the authentic information and questions. This will be useful to give justification and opportunity to MSMEs to becoming NPA and wilful defaulters without their mistakes.

- To publish the data of number of customers, borrowers and NPA MSME enterprises on the websites of public undertaking, private, foreign banks, multi-state cooperative, NBFCs and multi-credit societies to showcase their efforts & credibility towards MSME empowerment & their strength. Similar data should be published on IBA website.

- To consider branding, marketing and promotional financial support to brand and market the products and services at the national and international levels by participating in the various exhibitions, advertisements, conferences and B2B to build a brand to attract more customers and enhance the sales.

- To advice all financial institutions to exempt the personal guarantees from the entrepreneurs of the MSME sector, applying for financial support under the CGTMSE.

- To avoid considering the CIBIL report of the directors of the MSME enterprises, those who are having issues related to credit card and personal loan repayments. It should not impact while sanctioning the business loans related to MSME.

- The financial institutions should set up online portal or mechanism to answer the queries related to CIBIL, repayment schedule or wrong information or outdated information should be modified for avoidance of the rejection of the business loans.

- To provide trade, vendor, supply chain, exports, imports and equipment finance for a longer period without any hurdles and with low rate of interest.

- To bring out the unique settlement schemes for struggling / NPA units to continue their business activities and contributions.

- To provide loan facilities to the enterprises, who have completed 2 years in NPA regime.

- To reduce service and bank charges imposed on MSMEs without any conditions.

- To exempt the processing fees while sanctioning the loans to MSMEs.

- To consider credit facilities or loans upto 90% to buy industrial land and ready-made industrial premises to enhance manufacturing activities.

- To issue exclusive SME Credit Card and debit card for their current and loan accounts for making business payments or carry out business transactions.

- Not to impose any pre-payment penalty and other charges for business loans, term loans, industrial and commercial property loans, equipment and vendor finance.

- To create awareness about financial products and services for the benefit of MSMEs.

- To wave the interest element while settling the NPA issues of MSME sector.

- To include subject matter on a priority basis in the SLBC meetings and review the credit flow and resolution of issues and grievances of manufacturing and SME sectors.

- To advise the Regional Directors of RBI to include MSME agenda (review of credit flow, NPA restructuring, revival of sick units and affordable financial products) in the SLBC meetings organised under the Chairmanship of the Chief Ministers of each State. Also to resolve the NPA units with the help of State Governments situated on the Government industrial lands, so that the same industrial land can be utilised for other enterprises for manufacturing activities.

Mr. Salunkhe has also submitted his request to Dr. Joshi to organise official meeting with MD and CEOs of financial institutions including Public Sector, private & foreign Banks and leading NBFCs to take view of their efforts, lack of approach towards MSME sector and their issues & grievances at the earliest on a priority basis.

Regards

Maheshkumar

Director

SME Chamber of India

Mobile No: +91-7506046755

Email: maheshkumar@smechamber.com

« Delayed payments to Micro and Small Enterprises- A SolutionCredit Card Rules: Big news! RBI issued new rules related to credit card bill, Details here »

Related Posts

SEARCH SME E-News

RECENT POST

Archives

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

Categories

- Achievements

- Banking & Finance

- Branding & Marketing

- Business Ethics & Culture

- Business talk

- Business Tycoons

- Capital Market

- Corporate Story

- Davos

- Economy

- Emerging Market

- Entrepreneurial Leadership Dialogue

- events

- Exports

- Grievances

- Growth

- Impact on Business

- Import

- India Growth Story

- Industry

- Innovation and Invention

- Innovative Ideas

- International Affairs

- International Trade

- jobs career

- Manufacturing

- Meeting

- MSME

- Others

- Packaging

- Pharma

- Policies & Schemes

- Regulatory Change

- Schemes

- Skill Development

- SME Talks

- Start-up

- Swot Analysis

- Tax

- Technology & Research

- Textiles

- Travel

- Uncategorized

- Viksit Bharat 2047- Strategies, Contribution, Initiatives and Efforts

- Women Entrepreneurs

- World Economic Forum